Switch to Munim: Financial Accounting Software Migration Guide

AuthorMehul Jagwani

AuthorMehul Jagwani Reviewed ByCA Ajay Savani

Reviewed ByCA Ajay Savani

Not all financial accounting software is scalable; some software does not provide scalability as required, especially terminal-based accounting software. Thus, to address the requirements of your growing business, consider switching to modern and scalable accounting software with the capabilities of GST return filing.

In this blog we will discuss steps to migrate your financial software easily without hampering operations. Keep reading!

3 Finance Accounting Software Migration Approaches

When it comes to migrating from one financial accounting software to another, businesses often face challenges. To make this process smoother, companies typically adopt one of three approaches: phase-wise adoption, concurrent operations, or one-go transition. Each approach has its own benefits and considerations, so it's important to understand them in-depth before making a decision.

Phase-wise Adoption

Under this approach to implementing new financial accounting software in your company, the transition happens in chunks. Essential modules are given top priority. This approach is suitable for employees' peace of mind. It gives them enough time to prepare, but the transition cost is relatively higher.

Concurrent Operations

Concurrent operation is considered one of the safest and most secure approaches to implementing new financial accounting software. Under this approach, both systems are used in parallel.

The main advantage of this system is that a company can reverse the implementation anytime if something goes wrong. The drawback of this approach is that it requires additional investment and a larger workforce to maintain the old system.

One-go Transition

In this approach, the transition happens all at once. When the transition is being planned, a date is notified to all the departments. From that date onward, a new system is used. In exceptional cases, one can refer to an old system (e.g., to retrieve data).

If something goes wrong in the new system, it can create operational delays and may lead to a stressful work environment. Although the transition cost is the lowest among other approaches, it is risky, especially for large enterprises and MNCs.

Steps to Implement New Accounting Software

Setting up a new accounting system is not that difficult, so don’t feel overwhelmed. Following are the steps to set up a new financial accounting software:

- Open a New Bank Account

When setting up a new accounting system, the first step should be opening a separate bank account for your company. If you already have one, you can skip this step.

For the following reasons, you should have a business account:

- Keeping personal and business finance separate

- Organize business records easily

- Forecast cash flow

- Adheres to professionalism and credibility

- Simplifying tax returns

- Legal Requirements

Things you should consider before opening a current account:

- Reputation and stability of the bank

- Consider account opening fees

- Check minimum balance requirements

- Check the availability of additional services such as online banking, mobile banking, bill pay and overdraft protection

- ATM network

- Convenience of branch location and relationship manager

- Interest rates

- Quality of customer service

- Availability of additional services such as business loans

- Choosing the Right Accounting Software

Choosing the right accounting software for your business is a crucial decision. It's important to consider the features of accounting software and how they align with your business needs. To simplify your decision-making process, let’s categorize accounting software into two types: terminal-based and cloud-based. Each has its own advantages and disadvantages, so it's essential to choose the one that best suits your business requirements.

Whichever type of accounting software you choose, you need to keep a few other considerations in mind. Make sure that your accounting software:

- Billing/invoicing capabilities

- Inventory management features

- Offers GST compliance

- Supports multi-user

3. Setting Up Charts of Accounts

A chart of accounts is a framework for categorizing the financial data of all accounts employed by a business. In other words, it is a systematic approach to recording assets, liabilities, expenses, income, and equity.

Steps to set up different charts of accounts:

- Identify the main financial category

- For easy identification, assign a unique code to each chart of accounts

- Create a group of similar accounts with a logical hierarchy

- Give clear and descriptive naming

- To ensure completeness, review everything carefully before submitting to higher authorities

How to Setup Munim for your Company

Step 1 - Visit www.themunim.com and go to sign up page

Step 2 - Sign up by providing your mobile number and authenticate the same with OTP

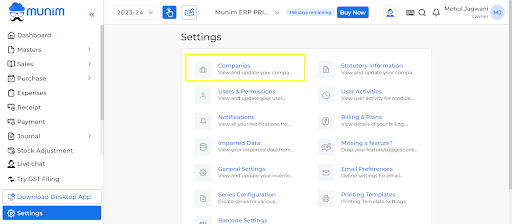

Step 3 - After signing up, go to ‘settings’, and then ‘companies’.

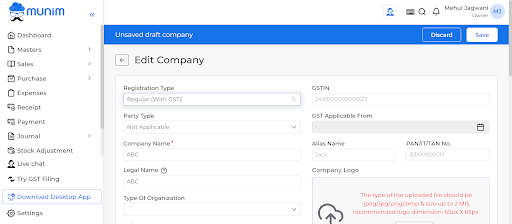

Step 4 - Update your company details.

These were the basic steps to set up your company accounting in Munim. Once you are done with these steps, you can proceed to creating charts of accounts, setting up inventory, and so on.

However, you can make the setup process much faster and easier by importing data from your existing financial accounting software.

Getting Started with a New Financial Accounting Software

After familiarizing yourself with the accounting software transition process through this blog, we recommend considering Munim for your financial accounting software needs. Munim stands out as one of the best options in the market, offering not only a smooth migration process but also GST return filing capabilities.

Frequently Asked Questions on Financial Accounting Software

- What are the essential functions of the financial information system?

The following are the essential roles of a financial information system in an organization:

- Setting your business accounting

- Monitoring the cash flow

- Analyzing the financial data

- Aids in decision-making

- Generating financial reports

- What is migration in financial accounting software?

In the accounting system, migration is transferring financial data from an old accounting system to a new one.

- What features should you consider when choosing a new accounting software?

Before subscribing to any accounting software, you should check if the software provides the following features:

- Invoicing

- Inventory management

- E-invoice generation

- E-way bill generation

- GST return filing

- Bank reconciliation

Disclaimer: "This blog post is for informational purposes only. For specific tax advice related to your business, please consult a qualified Chartered Accountant or GST practitioner."

About the author

Related Articles

Explore the latest market news, useful resources for business, and Munim updates.