What is ITC Reversal in GST? What are Rules 42 & 43?

AuthorMehul Jagwani

AuthorMehul Jagwani Reviewed ByCA Ajay Savani

Reviewed ByCA Ajay Savani

In the complex maze of GST compliance, where each invoice and each credit entry is important, a small mistake can attract a huge penalty. Most of the businesses fall prey to claiming maximum Input Tax Credit (ITC), but only a few know that you may have to reverse ITC if certain conditions are not met.

In this blog, we shall discuss what ITC reversal is and the conditions under which ITC have to be reversed under Rule 42 & 43 of the CGST Act.

What is ITC Reversal in GST?

ITC reversal, in simple words, is reversing the credit that you previously claimed on your purchases. Under GST, input tax credit on business goods and services can be claimed. You have to reverse a part of that credit when you use those goods or services, in part, either for personal purposes or for the production of exempt supplies.

It is like a refund that you have to give back due to a failure to fulfil certain conditions.

Let’s understand with an example,

You are operating a manufacturing company and are buying raw materials of the value of ₹10,000,000, and you pay GST of ₹180,000. 80% of those materials are taxable goods, and 20% are exempt items. You can only claim ITC on the 80%. The other 20% of ₹180,000, i.e. ₹36,000, should be reversed.

Scenarios Where ITC Reversal is Required

| Applicable rule | Case | Reversal deadline |

| CGST Rule 37 | The recipient failed to make the payment, either partially or fully. | Within 180 days from the date at which the invoice was issued. |

| CGST Rule 37A | If the supplier fails to make the GST payment via GSTR-3B before 30th September of the following year. | Must reverse the ITC by 30th November following the end of the financial year. |

| CGST Rule 38 | Under special rules, 50% ITC to be reversed by banking and other financial institutions. | While filing regular returns. |

| CGST Rule 42 | Inputs for exempt supplies or utilized for personal purposes. | The reversal deadline depends on the specific situation, but it is generally periodic. |

| CGST Rule 43 | Capital goods were used for either exempt supplies or personal purposes. | The reversal deadline depends on the specific situation, but it is generally periodic and the reversal amount to be calculated using a specified formula. |

| CGST Rule 44 | Deals with cases where GST registration was cancelled or switched to a composition scheme. | In the case of opting for a composition scheme, file ITC-03 form. For any other cases, file REG-16 form. |

| CGST Rule 44A | Reversal of 5/6th of the ITC claimed on gold dores in stock as of 1st July 2017 | Generally, at the time of supply. |

| Section 16(3) | Depreciation claimed on the GST component of the capital goods purchased. | Depends on specific circumstances |

| CGST Section 17(5) | Mention ITC for ‘blocked credits’ | At the time of regular filing or maximum can be extended to the annual return filing date. |

| CGST Section 17(5)(h | Inputs used in the goods that were destroyed, lost or stolen | Depends on the occurrence of the event. |

Rule 42: ITC Reversal on Inputs/Input Services With Calculations

It is one of the important rules in the context of ITC reversal because it deals with cases where ITC is used for both taxable and exempted supplies, as well as personal purposes.

In the following, we shall understand how to do the ITC reversal calculation under CGST Rule 42.

Step 1: Segregation of Specific Credits:

T: Total input tax credit.

T1: Specific credit for non-business use.

T2: Specific credit for exempt supplies.

T3: Blocked credits under section 17(5).

Step 2: Derivation of Common Credit:

C1: ITC credited to the electronic credit ledger.

Calculated as: C1 = T – (T1 + T2 + T3).

T4: Specific credit for taxable supplies.

C2: Common credit left after attribution.

Calculated as: C2 = C1 – T4.

Step 3: Computation of ITC Reversal from Common Credit:

D1: ITC attributable towards exempt supplies.

D2: Deemed ITC for non-business purposes.

C3: Remaining eligible ITC.

Calculated as: C3 = C2 – (D1 + D2).

Suppose a business has the following values:

Total ITC (T): ₹1,00,000

Non-business use (T1): ₹15,000

Exempt supplies (T2): ₹10,000

Blocked credits (T3): ₹5,000

ITC credited (C1): ₹70,000

Taxable supplies (T4): ₹35,000

Calculations:

C1 = ₹1,00,000 – (₹15,000 + ₹10,000 + ₹5,000) = ₹70,000

C2 = ₹70,000 – ₹35,000 = ₹35,000

Assuming D1 = ₹10,000 and D2 = ₹3,000:

C3 = ₹35,000 – (₹10,000 + ₹3,000) = ₹22,000

The business can claim ₹22,000 as eligible ITC.

Rule 43: ITC Reversal on Capital Goods With Calculations

Rule 43 of the CGST Act deals with the reversal of ITC pertaining to capital goods. The rule outlines the condition under which ITC is to be reversed.

The condition and the calculation are as follows:

Category A: Nature of Use

ITC is eligible if capital goods are used for business purposes, including zero-rated supplies, but not for exempt supplies.

Category B: Proportional Use for Taxable and Exempt Supplies

If capital goods are used for both taxable and exempt purposes, you cannot claim ITC fully on the supplies.

ITC eligibility gets limited to their proportionate share of the usage in taxable activities.

Here is how you can calculate the ITC in the given conditions:

Tm: ITC attributable to a month (monthly filing).

Calculated by dividing the credit by 60, (Tc/60).

Tr: Aggregate value of exempt supplies during the tax period.

Te: Common credit attributable towards exempted supplies.

Calculated as: Te = (Tm × Tr) / F

Where F is the total turnover in the state of the registered person during the tax period.

Suppose capital goods have an ITC of ₹100,000. The business has ₹30,000 worth of exempt supplies and a total turnover of ₹10,00,000.

Calculations:

Tm = ₹100,000 / 60 = ₹1667

Te = (₹1667 × ₹30,000) / ₹10,00,000 = ₹50 (to be reversed monthly)

Initially, ₹100,000 is credited to the ledger, and ₹50 is reversed each month based on the exempt percentage used over the capital good’s useful life.

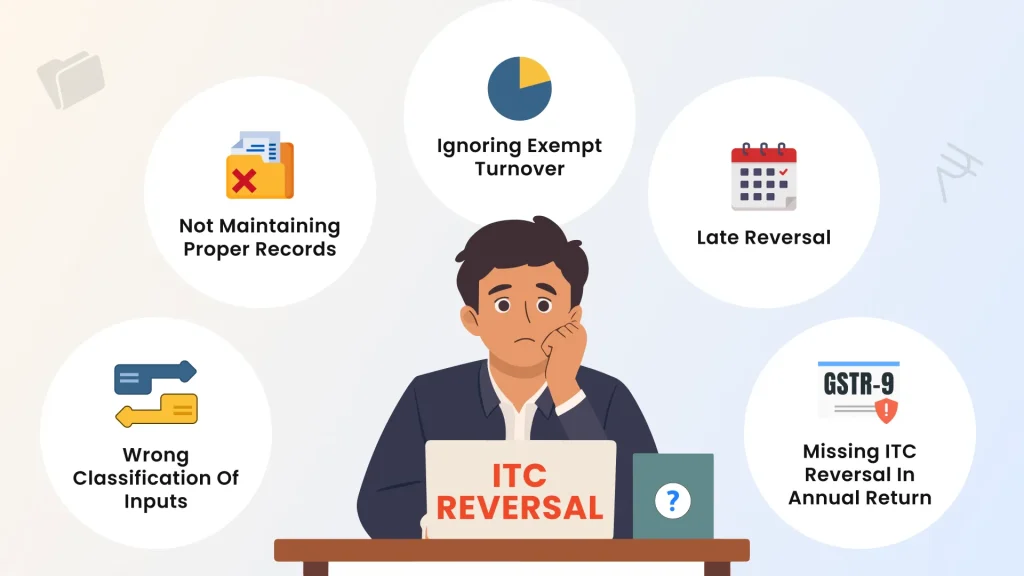

Common Mistakes to Avoid in ITC Reversal

- Ignoring Exempt Turnover: It is important to include exempt turnover; even minor exempt transactions should be counted when determining reversal.

- Late Reversal: Reversing ITC late attracts interest.

- Not Maintaining Proper Records: The most common cause of ITC disputes is a lack of documentation.

- Wrong Classification of Inputs: Misidentifying goods or services as exclusively taxable or exempt.

- Missing ITC Reversal in Annual Return: GSTR-9 requires you to reconcile reversal details.

Ending Notes

We hope that after reading this blog, you understand how to do ITC reversal and what rules 42 & 43 have with regard to the same. Timely reversal of ITC not only keeps your business compliant but also saves you from hefty penalties and additional interest payments due to late reversal. If you are a Chartered Accountant or a tax professional looking for GST return software, then you must try Munim GST Return Filing software. It has everything you need. Sign up now.

Frequently Asked Questions

How to reverse ITC wrongly claimed in GSTR-3B?

In case you have claimed ineligible ITC in the GSTR-3B, then you may reverse it in the same return or in any other monthly return.

How to reverse ITC in GSTR-9?

ITC reversal is reported in GSTR-9 (Annual Return) in Table 7 - Reversal of the input tax credit. Disclose the ITC reversed in the financial year, with reversals in the ITC reversal rules 42 & 43 and ineligible ITC identified later.

Disclaimer: "This blog post is for informational purposes only. For specific tax advice related to your business, please consult a qualified Chartered Accountant or GST practitioner."

About the author

Related Articles

Explore the latest market news, useful resources for business, and Munim updates.