Bank Reconciliation Statement: Everything You Should Know!

AuthorPriyanka Chaudhari

AuthorPriyanka Chaudhari Reviewed ByCA Ajay Savani

Reviewed ByCA Ajay Savani

- What is a Bank Reconciliation Statement?

- Importance of Bank Reconciliation Statement

- Who Prepare Bank Reconciliation Statements?

- 6 Steps that will Guide you to Prepare Bank Reconciliation Statement

- Bank Reconciliation Statement Format

- Munim Bank Reconciliation Statement

- Why Grab Munim Accounting and Billing Software for Bank Reconciliation?

- Key Takeaways

Reconciling bank accounts is not just a financial task- It is a crucial process to find and fix discrepancies between bank receipts and fiscal records. But what are your thoughts on bank reconciliation statements? Here’s a complete guide for you! Let’s unravel the insights into the topics and get clarity into your financial journey!

What is a Bank Reconciliation Statement?

A Bank reconciliation statement compares bank records with accounting documents to identify discrepancies and ensure precision. It reports unrecorded transactions, bank charges, cash balances, etc. The account reconciliation process caters to error detection and fraud prevention while ensuring financial clarity. Regular ledger reconciliation fosters businesses to eliminate mistakes, stay compliant, and clearly understand their fiscal health.

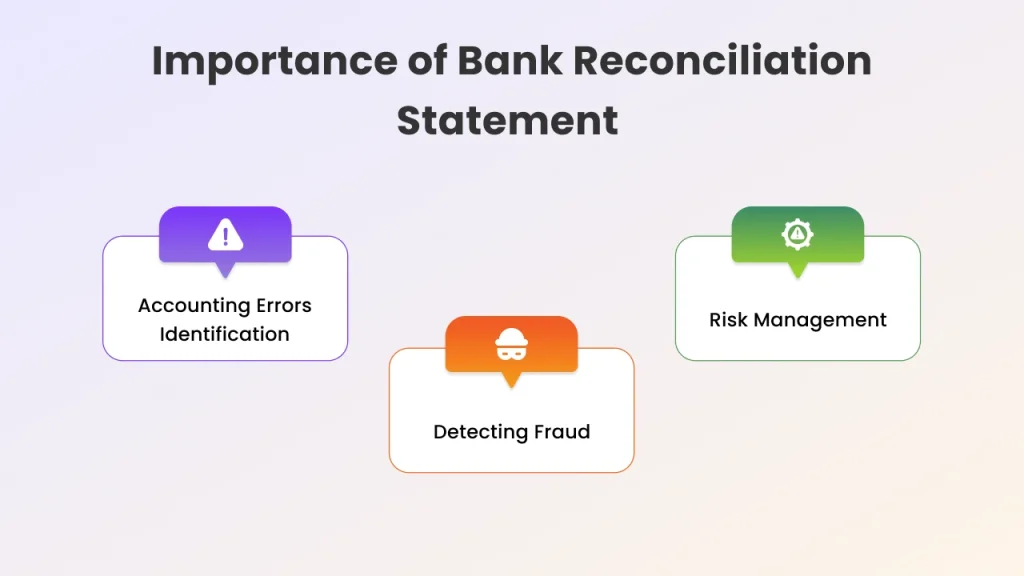

Importance of Bank Reconciliation Statement

- Accounting Errors Identification

Bank statement matching helps businesses validate that the payments were processed and the collected cash was deposited into the bank account. These statements generally identify unintended discrepancies, duplications, and simple errors. They are primarily used to find mistakes that are likely to have an adverse impact on financial and tax reporting.

- Detecting Fraud

Businesses prepare bank reconciliation statements to detect fraud, theft, and losses effectively. Consider that a cheque has been altered, and your payment is larger than the anticipated value. Reconciling your bank statements helps you identify these frauds and take corrective measures to recover the money.

- Risk Management

Bank records depict the company’s financial health for a particular time. Accuracy in these statements ensures investors or stakeholders make smart decisions. The statements give a complete scenario of their cash flows, which assists business owners in strategizing critical business plans.

Who Prepare Bank Reconciliation Statements?

A company wanting to compare its account balance with the one listed by the bank prepares a bank reconciliation statement. This statement depicts all transactions like withdrawals and deposits for a specified period.

6 Steps that will Guide you to Prepare Bank Reconciliation Statement

Bank Reconciliation ensures accounting records match the bank statements. You need to keep your bank statements for current and previous months ready before you start. Here’s a complete breakdown of the process. Here’s how you can get started:

- Get your bank statement copy for that time frame, your accounting or company ledger, list of deposits, payments, and cash balance from the accounting system.

- Begin by closing the balance for the preceding month, which will be your starting number.

- Examine all the bank documents, eliminating bank account details like cheques, transfers, and bank fees. Each statement must be recorded on your ledger or the accounting system. Make sure your deposits and cleared cheques tally with the values recorded in your bank statement. If these values incur an error, you need to review and record the missing or mismatched values.

- Now, review the bank transactions on the statements that are added to the account details. These include interests, transfers, deposits, as well as bank adjustments. Make sure, every positive transaction is reflected into your company ledger. If it isn’t, then you need to record missing values.

- As the bank reconciliation statement process comes to an end, make sure bank statement balance is equal to that of accounting records.

- For further discrepancies or errors, validate and check out the values being missed.

Bank Reconciliation Statement Format

Let’s check out the standard format for Bank matching statements.

- Add the name of the company or the individual holding the account.

- Date of statement issued

- Check your bank statements to enter the balance amount in the account.

- Additional details of bank statement balance. This caters to deposits in transit, interests earned, and that are not recorded by the bank.

- Get the adjusted balance from the bank statements.

- Add bank balance based on the company’s accounts.

- Deposits / credits reflected in the company records but not on the bank receipts.

- Add deductions from your company’s accounts.

- Add the signature of the designated person who has created the bank reconciliation statement.

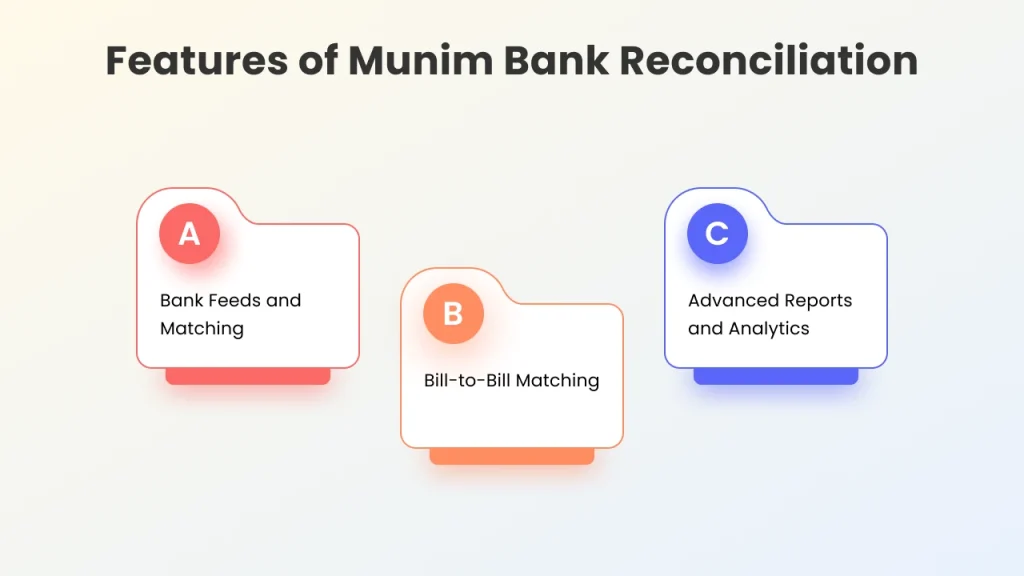

Munim Bank Reconciliation Statement

Say no to manual account reconciliations and ensure precision with Munim accounting and billing software! Here’s what we serve.

Bank Feeds and Matching: Our one-stop solution allows you to match your bank statements smartly while saving time and effort.

Bill-to-Bill Matching: Ensure bill-to-bill matching for modifications based on customer request.

Advanced Reports and Analytics: Get a reconciliation overview for matched and unmatched entries. This feature presents details of every reconciled entry, from date and time to bank history.

Also check How Munim Accounting Software Empowers CAs

Why Grab Munim Accounting and Billing Software for Bank Reconciliation?

- Remove Discrepancies

- Bank Integration

- Remote Collaboration

- Data Validation

- Reconciliation History

- Data Mapping

Are you surprised that one solution can offer so many perks and features? Then, you need to check out our accounting and billing software, your one-stop solution for all your accounting needs.

Key Takeaways

Bank Reconciliation Statement compares accounting records with bank statements to identify errors. It is important for identifying fraud, detecting accounting errors, and mitigating risks. You can follow the above steps to get started with bank reconciliation and use the format given in the blog. The easiest way to get started is with Munim accounting and billing software. Start reconciling your bank accounting with the best-in-class features we provide.

Use our comment box below to fire your queries. We will surely answer them.

FAQs

What is the journal entry for a bank reconciliation statement?

Accounting adjustments necessarily made to ensure cash balance which is specified in a company’s accounting records to match the bank’s cash balance is termed as bank reconciliation entry.

What is a reconciliation entry?

Reconciliation facilitates an importer to revise a few details of an entry summary that were not determined while entering merchandise information.

What are unpresented cheques?

Unpresented cheques in bank reconciliation statements are referred to as outstanding cheques because of the outstanding funds they hold. This means the cheque is written and accounted for but is not paid out by the bank for which the money is withdrawn.

What is reconciliation?

Reconciliation refers to an accounting process that compares two different sets of records for validating the accuracy of figures. This ensures the consistency of accounts in the general ledger.

Disclaimer: "This blog post is for informational purposes only. For specific tax advice related to your business, please consult a qualified Chartered Accountant or GST practitioner."

About the author

Related Articles

Explore the latest market news, useful resources for business, and Munim updates.