The Ultimate Guide to NRI Account Types in India

AuthorPriyanka Chaudhari

AuthorPriyanka Chaudhari Reviewed ByCA Ajay Savani

Reviewed ByCA Ajay Savani

Residing abroad doesn’t mean that you lose complete control over Indian finances! Thinking of managing your finances in India from overseas? You are not the only one. Millions of Indians settled abroad, raising the need to have a swift banking facility like never before. That’s where an NRI account comes into play- it’s a financial gateway that bridges the gap between cross-border income and Indian milestones.

It doesn't matter if you transfer money back to your home turf, wish to invest in Indian stocks, or plan to safely deposit your international earnings; deep diving into types of NRI accounts is important. The terms like NRE, NRO, and FCNR buzzing around – make it look a bit overwhelming. This article is a complete guide for you if you are living abroad.

What is NRI Account- Here’s a Nugget of Wisdom!

Specialized banking solutions tailored exclusively for Non-residents of India to process their financial ties in the country while living overseas is termed as NRI account. These specialized banking accounts are accessible only to those individuals who spend maximum days of the year in another geo-location out of the country. To open the account, the prerequisite criteria is that the individual must have spent at least 120 days of every year for a minimum of 4 consecutive years in another country. That’s because only then did the residential status change to Non-resident Indian under the IT Act 1961. However, individuals migrating to another country for employment are titled NRIs immediately.

Another requisite under budget 2020 says the person must have resided in India for less than 4 years out of the 10 previous ones to be categorized as an NRI. To manage their finances while overseas, it becomes crucial for these individuals to understand the features and benefits of NRI bank account in India.

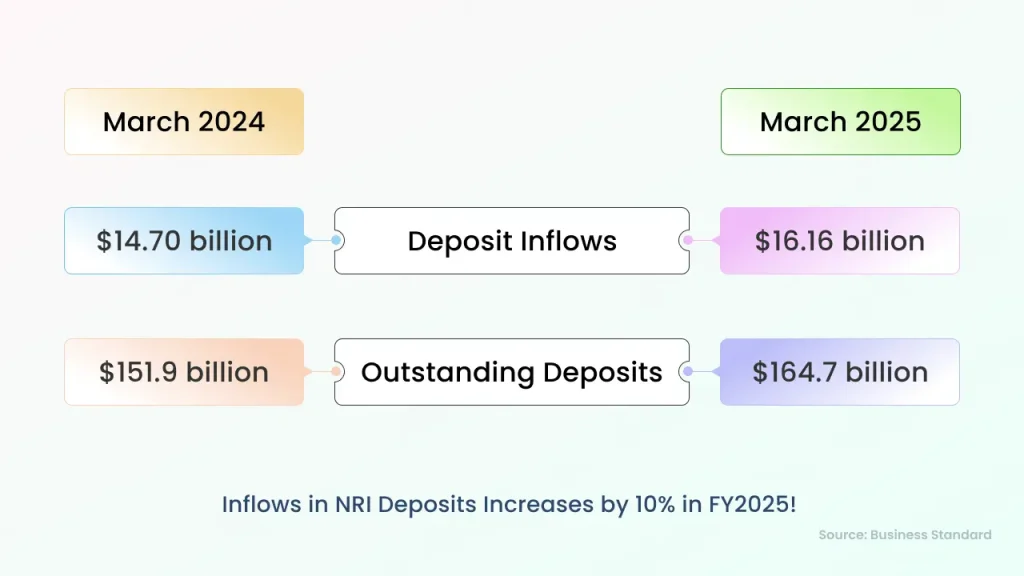

Inflows in NRI Deposits Increases by 10% in FY2025!

Now that we have understood the definition and prerequisites, it’s time to understand the types of NRI bank accounts. Let’s scroll down to get them in detail.

Types of NRI Bank Account- A Quick Snapshot!

- NRE Account- Non-residential External Account

- NRO Account- Non-residential Ordinary Account

- FCNR Account- Foreign Currency Non-residential Account

What is NRE, NRO, and FCNR Account?

1. Non-residential External Account!

NRE (Non-residential External) Account is your one-stop solution to transfer your global earnings to India. This NRI account facilitates individuals residing abroad to deposit income earned in foreign currency but in the Indian “Rupee” denomination.

NRE Deposits in India!

Let’s consider an example! Raj is an NRI working in Paris, France! His Parents are retired and are completely dependent on him; they reside in Delhi. Every month, he deposits 3000 Euros in his NRE account, which is converted to Indian rupees. Considering the exchange rate as 1 EUR= 85 INR, his NRE account holds 2,55,000 in Indian rupees.

Also, NRIs can skip ITR filing in India if their total income in the country is below the taxable limit and no TDS refund is claimed. Learn more about the conditions for NRI exemption from ITR filing.

2. Non-residential Ordinary Account!

A Non-Residential Ordinary (NRO) Account is your financial hub within India that facilitates you to seamlessly manage the money earned within the country, irrespective of where you reside. The income source for this NRI account is either rental money from the property, pension, or other incomes earned in India, which you wish to manage from cross-borders.

NRO Deposits in 2025!

Let’s consider that Shamita is an NRI working in the USA and has a shop in Surat, which is rented by a retailer, Mr. Patel, for ₹15K per month. To receive and manage this rental income, Shamita needs to open an NRO account, where Mr. Patel transfers ₹15K every month. As the income earned is already in Indian rupees, there’s no currency conversion.

3. Foreign Currency Non-residential Account!

A foreign Currency is a Non-Residential (FCNR) Account, which refers to a fixed deposit account in India facilitating NRIs to transfer their abroad-earned income directly to the Indian bank. Eliminating the need to convert it into Indian currencies, this NRI account accepts deposits in universally accepted international currencies like USD, EUR, and more. The perk that adds to this NRI bank account is that the deposits grow at the Indian rate of Interest without being depreciated with the rupee.

FCNR Deposits in 2025!

Let’s consider an example: Diya works at Amazon in New York, USA and wants to deposit $2000 every year to her Indian bank account. The money will not be converted to INR but will be directly deposited to her FCNR account in India.

Which NRI Account is the Best for You?

Talking about the best NRI account in India for you? It all narrows down to purpose- totally depends on why you need it.

- Go with an NRE account if you wish to transfer foreign income to India with tax-free Interest and in Indian currency.

- An NRO account is the best fit for you when you wish to manage your income earned in India while you reside out of the country.

- Planning for no currency risk? FCNR is the best choice, which facilitates you to hold FDs in foreign currency for a long period.

Let’s Conclude!

Residing overseas doesn’t mean you are pushing your Indian finances to autopilot mode. It’s all about choosing the right NRI account to manage your finances seamlessly, right from wealth to investments- from across the globe.

We have seen types of NRI accounts, and each one serves a different purpose. The catch to choosing the best one is identifying your financial goals and verifying if the account matches them.

Check this out 7th Central Pay Commission

FAQs on NRI account!

1. What are NRI Account Benefits?

- Easier transfer of funds

- Seamless access to loan facility

- Effortless currency conversion

- Secure fund storage

2. Who is Eligible for an NRI Account?

An Indian citizen might be a student, working professional, or an individual on a vocation residing out of the country is eligible for NRI bank account.

3. Can I directly deposit INR in an NRE account?

No, you can’t directly deposit INR in an NRE account.

4. What is the minimum balance required for an NRI account in India?

The minimum balance requirement completely depends on the bank and types of NRI account.

Disclaimer: "This blog post is for informational purposes only. For specific tax advice related to your business, please consult a qualified Chartered Accountant or GST practitioner."

About the author

Related Articles

Explore the latest market news, useful resources for business, and Munim updates.