How Pending Credit Notes Impact GST Compliance and ITC Under IMS

AuthorMehul Jagwani

AuthorMehul Jagwani Reviewed ByCA Ajay Savani

Reviewed ByCA Ajay Savani

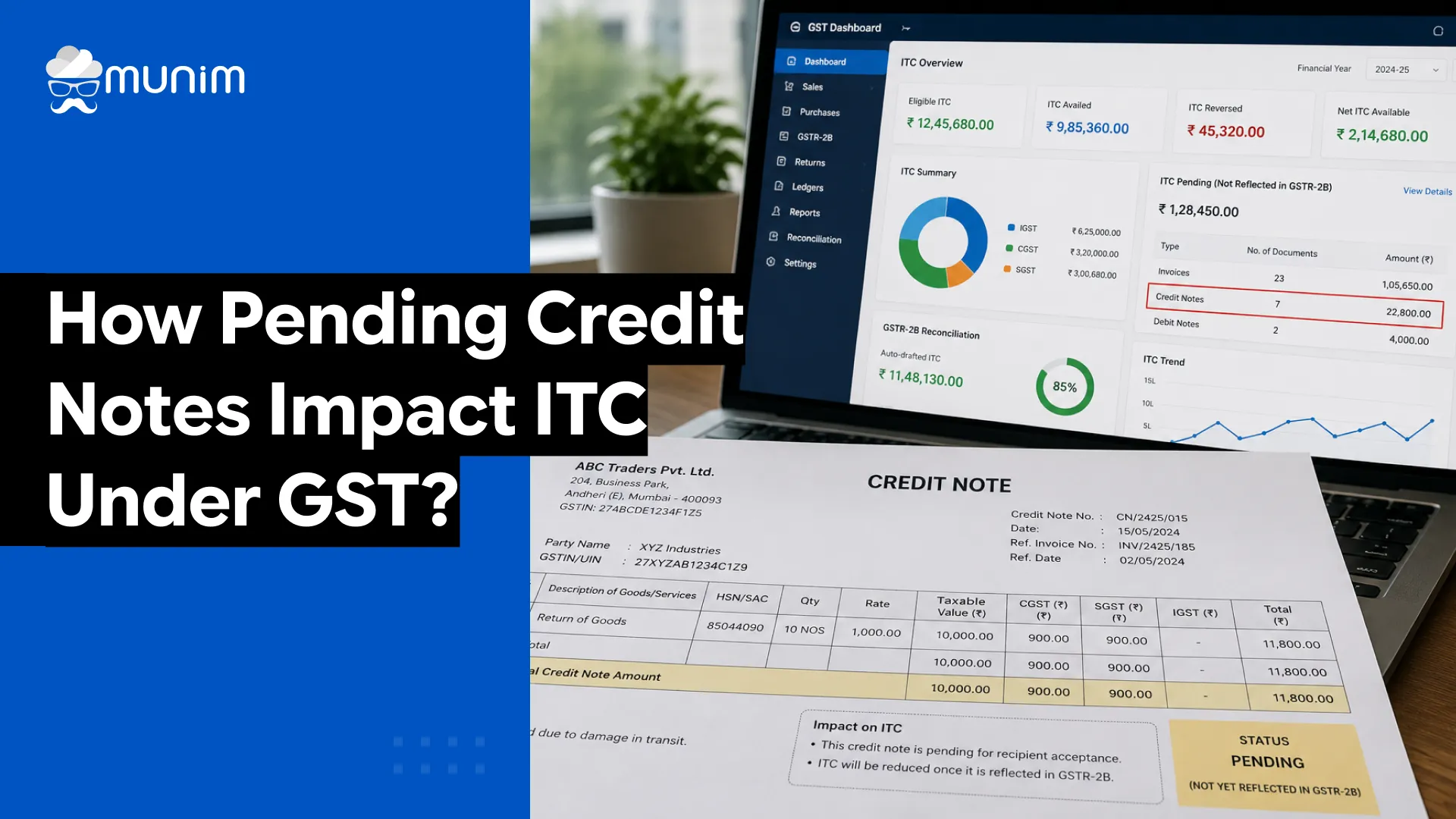

Pending credit notes under GST are not just a bookkeeping concern. They directly affect how much Input Tax Credit a business can claim, how accurately GSTR-3B gets filed, and whether the GST department sends a notice. With the Invoice Management System now active on the GST portal, every GST credit note issued by a supplier lands on the recipient’s dashboard and demands a clear action — accept, reject, or pending. Businesses that ignore this are sitting on a compliance risk they may not discover until it is too late.

What Is a GST Credit Note and Why Does It Matter?

A GST credit note is a document issued by a supplier to reduce the value of an earlier invoice. This happens in several situations: goods are returned, the original invoice had an error, a discount is given after the sale, or the agreed price changes after billing.

Under Section 34 of the CGST Act, when a supplier issues a credit note, they reduce their output tax liability in GSTR-1. This reduction directly flows into the buyer’s GSTR-2B. If the buyer had already claimed ITC on the original invoice, that ITC now needs to be reversed — at least partially.

The problem? Before IMS came into the picture, this entire process was manual, error-prone, and invisible in real time.

To understand the full distinction between debit and credit documents under GST, see our guide on debit note and credit note differences.

How Did Pending Credit Notes Work Before IMS?

Before the Invoice Management System was introduced, the workflow was straightforward on paper but chaotic in practice.

Here is how it typically played out:

- Supplier S issues a credit note of Rs. 50,000 (with Rs. 9,000 GST) to Buyer B.

- The credit note appears in Buyer B’s GSTR-2B on the 14th of the following month.

- The system automatically reduces B’s ITC in Table 4A(5) of GSTR-3B.

- If B had already claimed full ITC and the credit note was incorrect, B had to manually reverse the ITC in Table 4B(2).

This created three major problems.

First, Buyer B bore the administrative burden of catching and correcting someone else’s mistake.

Second, if B missed the reversal, GSTR-3B would show an incorrect ITC claim, leading to a demand notice from the GST department.

Third, the government had no invoice-level visibility into whether the credit note was legitimate. Revenue loss due to incorrect credit notes went undetected until a notice was issued.

The GSTN had no mechanism to flag whether a credit note was accepted, rejected, or even reviewed by the recipient.

Designed for Modern Tax Professionals

A premium filing solution for CAs and tax consultants who need speed, scale, and operational clarity.

Handle multiple clients with ease

Handle multiple clients with ease- Reconcile and validate with confidence

- Overcome the limitations of the GST portal

How Does IMS Handle Pending Credit Notes Today?

Under IMS (Invoice Management System), the moment a supplier issues a credit note and reports it in GSTR-1 or the IFF, it becomes visible on the recipient’s IMS dashboard. The recipient can take one of three actions.

Accept: The credit note is correct. The ITC reduction is applied in GSTR-2B and flows into GSTR-3B.

Reject: The credit note is incorrect or does not belong to the recipient. Rejecting it prevents the credit note from appearing in GSTR-2B and stops any automatic ITC adjustment.

Pending: As of the GSTN advisory dated 23rd September 2025, certain records can be kept pending for one tax period — one month for monthly filers and one quarter for quarterly filers.

The records eligible for the pending status include:

- Credit notes, or upward amendments of credit notes

- Downward amendments of a credit note where the original credit note was already rejected

- Downward amendments of invoices or debit notes only where the original invoice was already accepted and GSTR-3B has been filed

- ECO documents (downward amendments) where the original was accepted and GSTR-3B has been filed

Businesses must note that keeping a record pending for more than one tax period is not allowed. If no action is taken within the allowed period, the system may auto-populate the record into GSTR-2B based on default behaviour.

Real-World Example: Credit Note Handled Under IMS

Consider this scenario. Supplier S issues a credit note of Rs. 50,000 with GST of Rs. 9,000 to Buyer B, dated 1st January 2024. The credit note number is CN001.

Without IMS:

The credit note flows into B’s GSTR-2B on 14th February 2024. B’s ITC is automatically reduced in Table 4A(5). On 15th February, during reconciliation, B noticed the credit note was incorrect and manually reverses the ITC in Table 4B(2) before filing GSTR-3B on 20th February. This adds unnecessary compliance work to B’s plate, and the government has no invoice-level insight into the error.

With IMS:

On 1st January 2024, B received a real-time notification about CN001 on the IMS dashboard. B reviews it immediately and rejects it. Since the rejection happens before GSTR-2B is generated on 14th February, the credit note never appears in B’s GSTR-2B. There is no automatic ITC reduction and no need for manual reversal. GSTR-3B is cleaner, and B files without any adjustment burden.

Final Thoughts

The introduction of IMS has made the handling of GST credit notes more structured and more accountable than ever before. Pending credit notes are no longer silent threats that create reconciliation problems months later. They are visible, actionable, and time-bound under the current framework.

For businesses and Chartered Accountants managing multiple GST registrations, the takeaway is clear: do not let credit notes sit unreviewed on the IMS dashboard. Set up a regular review cycle, assign clear ownership, and make use of the rejection remarks feature to keep communication with suppliers smooth. Mismatches that go unresolved can also show up as GSTR-3B and 2A mismatches, which carry their own compliance consequences.

Frequently Asked Questions

1. Does a pending credit note affect GSTR-3B automatically?

Under IMS, a credit note impacts GSTR-3B only after it is accepted by the recipient. A rejected credit note does not appear in GSTR-2B and therefore does not affect GSTR-3B or ITC.

2. What should a buyer do if they receive an incorrect credit note?

The buyer should reject the credit note directly on the IMS dashboard. This prevents the credit note from flowing into GSTR-2B and affecting ITC. The rejection also notifies the supplier to take corrective action.

3. Can a buyer partially reverse ITC on a credit note?

Yes. Under the new IMS facility, a recipient can declare the exact ITC availed and reverse only that specific portion — either partially or fully.

4. What is the impact of GST credit notes on the supplier’s tax liability?

When a supplier issues a credit note, they can reduce their output tax liability in GSTR-1.

5. What happens if a supplier does not act after a buyer rejects a credit note?

The mismatch between the supplier’s GSTR-1 and the buyer’s GSTR-2B persists. The supplier may face notices from the GST department for under-payment of output tax liability.

Disclaimer: "This blog post is for informational purposes only. For specific tax advice related to your business, please consult a qualified Chartered Accountant or GST practitioner."

About the author

Mehul is a seasoned content writer with a passion for simplifying complex accounting and GST topics. With a keen interest in entrepreneurship and business management, he specializes in creating informative and engaging content for themunim.com. His goal is to help businesses understand and implement accounting and GST software solutions effectively. When he's not crafting content, Mehul enjoys exploring new places and spending time with his Golden Retriever.

Related Articles

Explore the latest market news, useful resources for business, and Munim updates.